Two weeks ago I wrote a piece about how financial independence and retiring early doesn’t have a rule book. As the FIRE movement has become more popular in the mainstream in recent years, it’s had to fit into soundbites. The ideas have lost some of their nuances.

This post serves as a follow-up to that article which highlighted the aspects of FIRE that spark disagreement. Those were:

- Defining a safe withdrawal rate (4% rule)

- Relative spending (destitution vs. luxury)

- Debt and emotion

- Defining “retirement”

- Relationships and money

- Costs of raising children

I argued that there’s a broad range, a spectrum, that we all fall along in regard to each of these topics as we pursue reaching financial freedom.

We do it differently—FIRE is unique to each of us. I suggested that FIRE has no hard and fast rules.

What I want to talk about today is how FIRE’s growth and siloing might be fracturing the movement. We often treat it like there’s a “right” and “wrong” way to tackle our relationship with money, debt, investing, and saving. Forum posts and comments are written as absolutes. Articles leave little room for discussion and often prescribe a specific strategy. Real estate investing is the smartest play. Or index funds are the only way.

How has FIRE evolved to reach this point?

FIRE’s Evolution

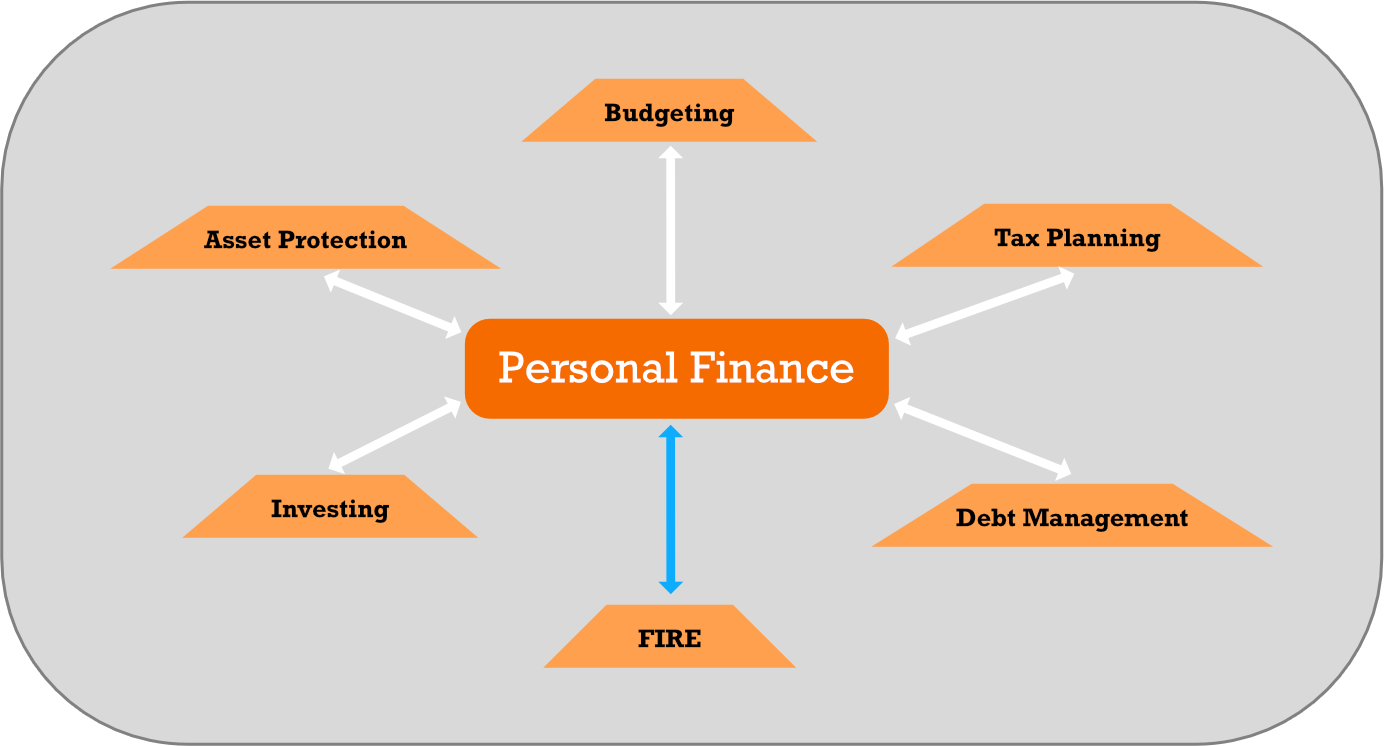

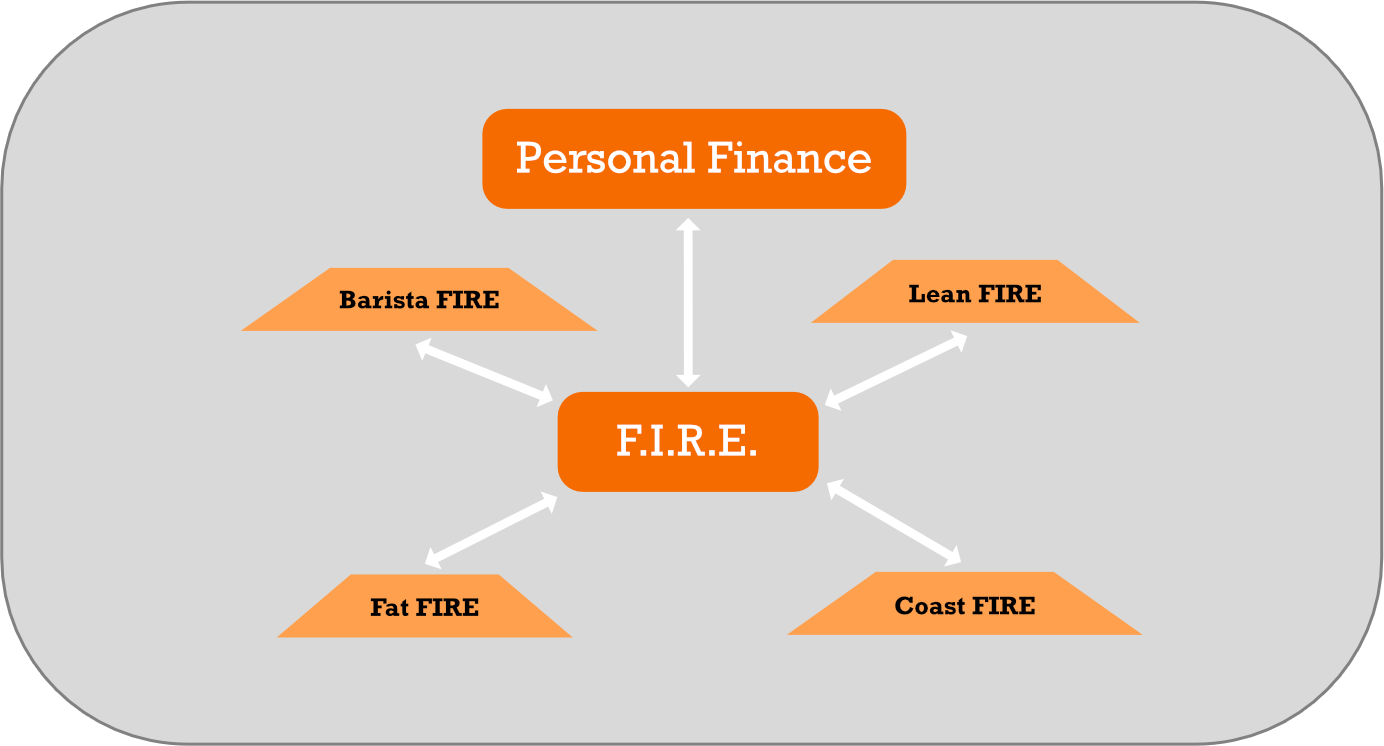

As I see it, FIRE came about as a “subcategory” of personal finance discussion and writing.

It sat alongside subtopics like budgeting, tax planning, and debt management.

It branched off like this:

While the core concepts of modern FIRE sprouted from Your Money or Your Life (1992), they didn’t start to become culturally widespread until they reached the web. Early Retirement Extreme, the story of a man (and eventually, a couple) living in an RV on $7,000/year/person, brought the notion of FIRE to the masses in 2007.

Over time, a community developed around FIRE. It became “the FIRE movement” in the mainstream media. It was no longer just a couple of crazy bloggers pursuing FIRE, but also regular everyday people. FIRE began to encompass more than just the science and numbers behind the financial concepts. It became a lifestyle. Mr. Money Mustache and Mustachianism flourished in the mainstream media.

The community exploded and now the multitude of discussion, strategies, and situations encompasses nearly every possible iteration and stretch much further than personal finances.

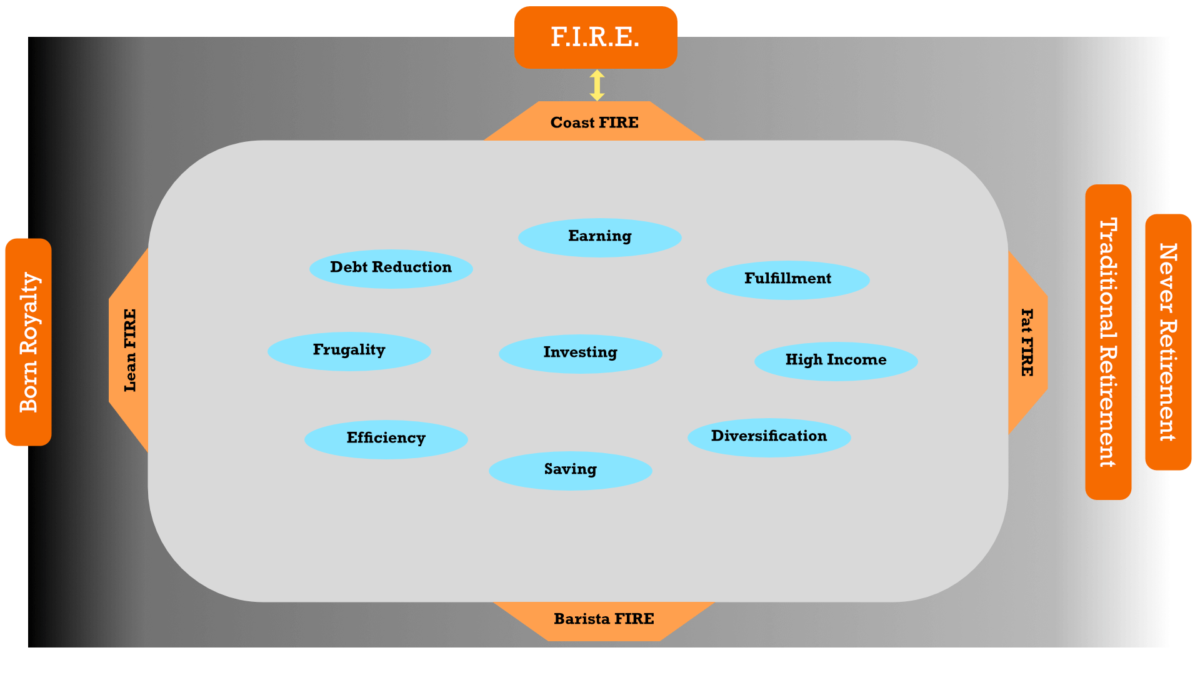

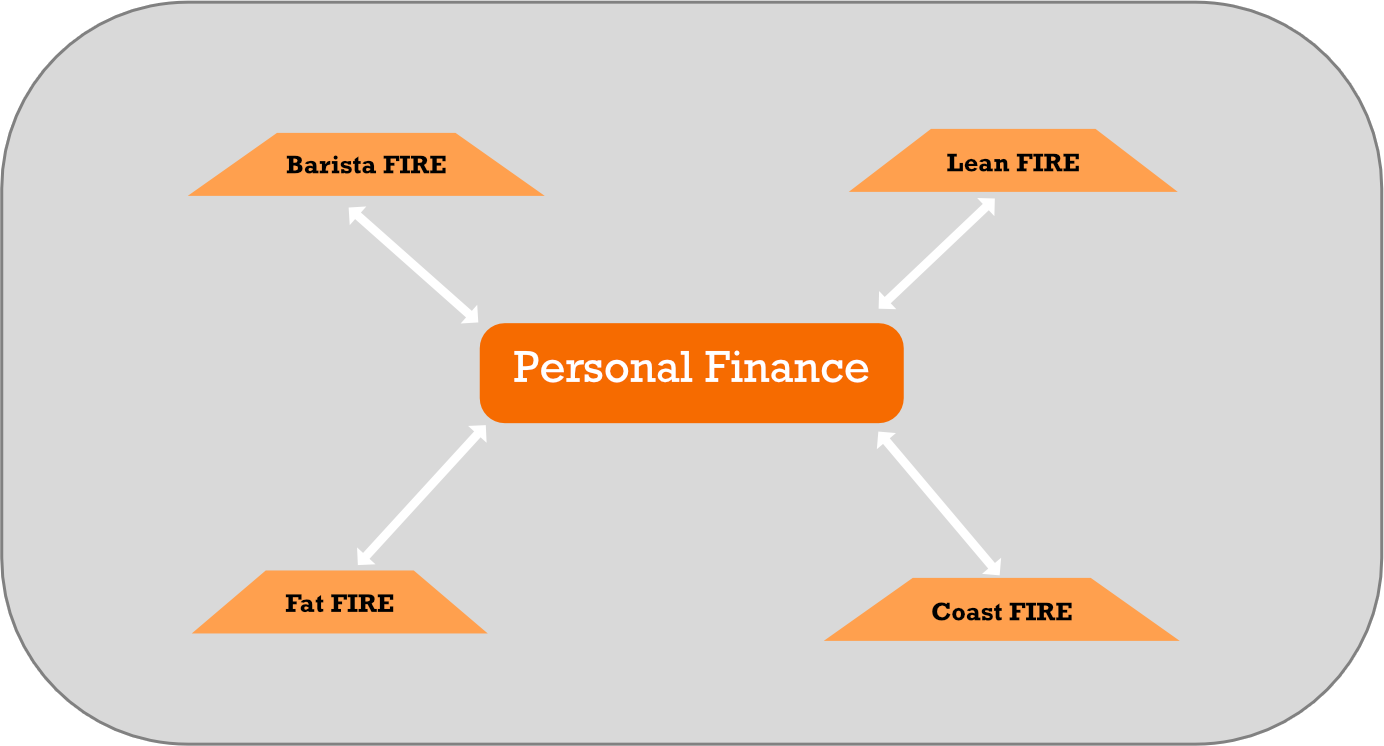

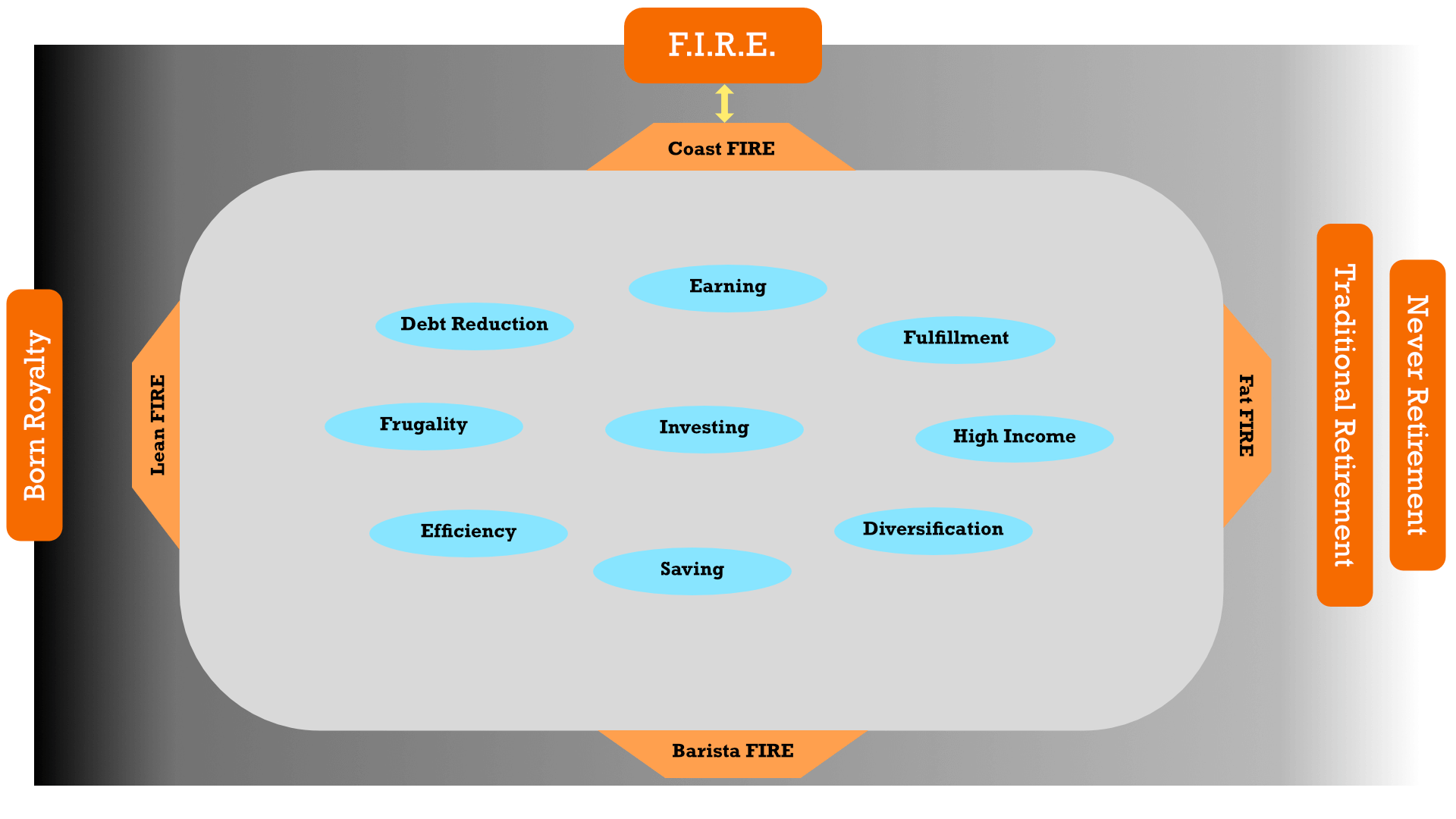

The different types of FIRE

With this growth, FIRE has broken down into several “types” with their own communities.

FIRE has evolved.

You might be familiar with some of the FIRE communities:

- Lean FIRE—retire with household expenses of $40k/year or less

- Fat FIRE—retire with an upper-middle-class lifestyle, perhaps $100k/year or more

- Coast FIRE—enough in retirement accounts that’ll cover traditional retirement, so you need to work enough to cover current expenses only

- Barista FIRE—by working part-time, low-stress job and drawing down investments, you can cover your expenses into perpetuity

That’s just to name some of the bigger ones. There are subreddits, blogs, and forums dedicated to just these types of FIRE.

But, the problem, as I see it, is that as FIRE has grown—so too has our identification with these dispirate groups.

We find ourselves in silos, reading the blogs and forums that support our different FIRE ideologies. Our membership in these groups make us identify the others as “them”.

We’re no longer on a path to FIRE.

We’re on the road to Fat FIRE or Lean FIRE.

As a FIRE community, we’ve become more siloed. More separated. And more against each other’s viewpoints. And it breeds negativity.

I’m not the only one that sees it this way:

Pay off house? Fool.

Don’t pay off house? Fool.

Like just about anything else on the internet today, as a community, FIRE is becoming more polarizing.

The controversy algorithm

Twitter users set up straw men to argue against.

“Renting is just paying someone else’s mortgage.”

“You don’t own your house even if you buy it—banks do.”

Arguments rage back and forth over these finer details.

And unfortunately, it’s exactly how the modern social media landscape is designed to work:

When you target an ad to a certain Facebook audience, you’re actually bidding against other advertisers in an auction for that group’s attention. And Facebook openly tells businesses that the platform will “subsidize relevant ads,” meaning an ad can win an auction even against higher bidders if the algorithm deems it more relevant to a given user. Why? Because to keep selling ads, Facebook needs to keep users on the platform.

Businesses are incentivized to show users more of what they’re already interested in through these systems. If you want to expand your reach while keeping your ad rates down, you need to show users more of what they already agree with.

And while you and I aren’t businesses talking about FIRE, these studies shed light on the general algorithm used by social media companies. The space we all interact within—timelines, walls, and comments. They want to drive engagement and time spent on the platform—and that comes from showing people more and more of what they agree with or what riles them up.

Through myriad algorithms, we’re broken down into clusters and set into our own echo chambers.

Businesses take advantage in order to market to us in different ways. There’s a playbook to generate clicks and raise business revenue:

- Amplify a polarizing attribute.

- Drive a wedge in the market.

- Launch a provocative ad.

No really. Here’s how you too can make the most of a polarizing brand.

And you know it’s true. Do you know what generates clicks for bloggers, YouTubers, and media? Controversial titles. Clickbait.

It’s no wonder that ad and sponsor-fueled creators, paid in relation to how many eyes they can bring to a marketing plan, are incentivized to talk about the extremes, the controversial.

And it’s probably why few writers can get away with not talking in prescriptive absolutes or coming up with controversy.

Our incentive

It’s certainly possible to be a good writer, attentive to your reader’s best interest, and sell adjacent, useful products or services. It’s just much harder. And more rare.

For example, let’s look back at the controversial topic I opened the previous section with—homeownership.

I wrote a pair of articles that took me a few weeks (and over 4,600 words) to write. They dealt with renting and investing vs buying and deciding whether to pay off your mortgage or invest. Each of these articles is a nuanced discussion that acknowledges the pros and cons of either decision.

Neither concludes with a clear prescription or “right” way. They ask more of you, my reader. And while I think that’s what’s in your best interest, it’s probably not what’ll generate maximum shares or search traffic. It’s not simple or clickbaity.

But I only get to do that because TicTocLife isn’t beholden to sponsors or advertising. There’s no financial incentive for me to maximize traffic or slant the thread of an article. In fact, it costs us money each time you load up a page.

So why write this? Genuinely, it’s enjoyable to write and internally valuable to help lift others up to achieve what we have. After all, we have enough money.

The value is in the grey

The truth that applies to most of us is what’s in between black and white. It’s in shades of grey. That’s where you find the valuable discourse, insightful wisdom, and unforseen ideas.

People argue about the extremes—the black and the white. But those points only exist at the very ends, and they cover so little of what matters.

We agree way more than we disagree.

And while I think this sentiment applies to much more than FIRE, I think it’s important that we recognize it as the FIRE movement continues to grow and evolve.

Lean, Coast, Fat, Barista—they’re all shades of grey within the FIRE movement. They might dictate a different take on debt reduction or frugality for example, but their core focus is the same. FIRE’s purpose is to free yourself from the burden of financial obligations so that you can live your life in the way you choose.

If we think of being born with a silver spoon in our mouth as one extreme and never retiring from work as the other extreme—FIRE and its many subtypes sit in-between. They exist on a spectrum. And each has its points of discussion and variations on shared areas of interest.

Lean, Coast, Fat, Barista—and whatever other variation on FIRE you might find—all have the same shared DNA. Live below your means. Knock out unhealthy debt. Invest the rest. Repeat until work is optional.

We agree on way more than we disagree.

The Risk of Silos

Having different versions of FIRE lets each of us more closely identify with a subtype of the movement. Maybe we align with minimalism and sustainability along with anti-consumerism. You might find a home with Lean FIRE. Perhaps you want to live a typical American middle-class lifestyle and have an upper-class income to support it. Beamers and fine wine may not be your thing, but you still want the luxury of a smooth (somewhat new) ride and the occasional night out. Fat FIRE could be right up your alley.

These communities let us identify with others that share our interests. But they also risk us tuning out the new ideas of the greater FIRE community.

FIRE came about as a novel take on the traditional path through adulthood and retirement. Its creation came from melding different ideas together.

The next wave of lifestyle design will almost certainly come about from the pollination of ideas from different perspectives.

If we’re too siloed, too polarized, we might miss the forest for the trees.

The ultimate goal of the FIRE movement is to shed light on a lifestyle that might lead to more contentment and satisfaction for those that choose to follow it. The goal isn’t to quit working as much as it is to have the freedom to choose to do so.

By keeping our lines of communication open and receptive to these new ideas, we’ll be better prepared to ride the next wave to a better life.

What do you think about the current health of the FIRE movement?

What about its future? Let me know in the comments!

20 replies on “Is the FIRE Movement Fracturing Into Silos and Extremes?”

Love the post. I’m from the classic Mr Money Mustache days. Live below your means, invest excess funds and retire when 4% covers your expenses.

That’s it isn’t it?

Anyhow, I think the movement is doing fine. FIRE is still FIRE. Lean, Fat or anything in between.

As long as your in one of these categories you are a FIRE hero to me.

Cheers!

Hey BF! Glad to hear from you. Coincidentally, I’ve got your latest post up in another window—you’ve had a lot going on!

Yep, there’s really not a whole lot to the basics of FIRE. I think that’s why I’ve enjoyed writing about more of the psychology of building wealth and life to boot. Although there’s some fun in deep-diving on the financial questions, too (like the aforementioned buy/rent topic from this post).

And I hope you’re right about FIRE! I wonder what the 60s/70s counterculture movement/hippies would think of what’s become of that movement’s populous today?

Great take. I’m not even sure I fit into one of the FIRE categories you mention. I guess I’m between lean Fire and Fat Fire, if I were to try and label myself and use the 4% rule.

I do agree that the community can be an echo chamber. I find I really like reading contrarian opinions by other FIRE bloggers/authors. I don’t have any set rules for myself other than to try and keep an open mind.

Curious, where would you label yourself in the many categories of FIRE?

Noel! Nice to hear from you.

To be honest, I’d heard of the different types of FIRE in passing over the years, but never really self-identified with any of them. Hell, I have trouble identifying with “FIRE” often. I mean, I still do some work—though I mostly give the money away (either directly like our Reader Fund, or indirectly by ensuring the people I work with receive all of a project’s budget). And I don’t plan on not working, like, ever. But I don’t really define work the way most people do. I just think of it as productive activity. And I find a lot of purpose in that, even wrote a post about why I think people work [spoiler: it’s to create]. I find a lot of satisfaction in breathing something into the world.

So, I guess I definitely match up with the FI part. And if I get to define retirement as not working for money, I’m willing to roll with the RE part. Fat? Lean? I don’t know. We could spend a lot more money and never run out. Closing in on double what we do, in fact. But… I think we get more out of doing other things with that money, so we’ll do that.

No matter how confident us writers often sound, we’re all just struggling our way through finding out what life is to us. I have more questions than answers, still. 🙂

Thanks for this blog. I found this by MMM articles and really appreciate that you take the time and words to fully discuss an issue. Thank you for not filling up the space with a bunch of annoying ads. I agree there is so much more that people can agree on, so why focus so much on the little points where people chose to disagree upon. Keep posting I look forward to the next installment!

Oh, awesome you found us through the MMM app, Tim! Thanks for coming by.

A lot of Jenni and I’s writing is really just an excuse for us individually to explore topics we’re interested in. We want to learn and stretch our comfort zones. As writers, we bring you all along for the ride and hope there’s some insight—a piece of wisdom here or there—that adds to your life. Glad to have you along for the ride, Tim!

So far as ads… well, to be clear, there’s nothing inherently wrong with them! I definitely think authors deserve to get paid for their work on the web. And ads are a big way to make that economically viable. But I do think they offer an additional layer of friction to authentic writing. Some can manage that, some can’t. We’re fortunate we don’t have to, and that this isn’t a money-making endeavor. I count us lucky in that regard.

Cheers!

There definitely are different breeds of FIRE these days. Everyone is talking about how their breed of FIRE is better than other breeds of FIRE when really, all breeds of FIRE are good in their own ways.

Too much ego is never a good thing.

David,

I actually think that, at least in an ideal scenario, it’s pretty great to have these different categories of FIRE these days.

Ultimately, our aim (Jenni and I) is to try to expose more people to the idea of financial freedom and building a life you want. With that, we hope people will reconsider the life they’ve obtained and how they got there—perhaps helping out others less fortunate and guiding friends/family to their own versions of financial stability.

And it’s easier for us to do that when there’s more “directions” to point people toward with goals that match their own more closely. Fat, Lean, etc. offer that.

But indeed, I worry when they start grinding against each other as some of the tenets of the different FIREs don’t really match up. But, maybe we’ll end up with a stronger idea of what FIRE is at the end of it.

Great post, Chris. I love how you point out the diversion and fragmentation of FIRE. This was one of the biggest challenges I had when I was writing my book this past summer (The F.I.R.E. Planner). I had to determine what was relevant vs. what wasn’t, too much detail vs. not enough, etc. In the end, I agree with you. FIRE needs to be personal, although it’s great to have models readily available to reference. It’s about the FREEDOM to choose.

Hey Michael!

Indeed, writing out a “guide” to FIRE might be difficult when it comes to these different variations. I can see how it’d be tough to start from some sort of “main branch” and then try to classify people into one of the subcategories (Fat, Lean, Barista, etc.).

I think part of the problem is that the “main branch” isn’t super clear when a lot of the basics we might traditionally point to within FIRE (4% rule, the retiring part, etc.) butt heads with the tenets of the subcategories. Retirement might get thrown out the window, or the numbers might be a lot more/less conservative. I think that’s all OK but it makes the core “FIRE” part less clear.

Everyone has to find their own path in life. I don’t really care about the fracturing. It’s just everyone trying to find a way to make it work. We don’t really fit in any of those categories easily either. I guess it’ll be FAT fire once we stop working completely. Life is really good right now so I’m good.

Joe—

Yep, everyone needs to find their path. And life is certainly a kaleidoscope of values, goals, and desires. We all get where we need or want to be in our own ways.

We’ll see if we can all retain the “FIRE” part of the different variations, the part that keeps us together as a community. 🙂

Nice post!

One benefit of the silos: people don’t have to wade through negative remarks about the lifestyle they’ve chosen. Ex: fatfire people making negative comments about living lean and talking about how easy it is to achieve mid-six-figure incomes, sustainability-minded folks making comments about overconsumption, etc.

Yep, I agree with what you’re saying. It’s easier to “filter” out folks who might not match your own (or the group’s) goals and background.

But, that goes against the purpose of the post. Much of the focus is on breaking down those silos and having FIRE folks communicate more across different socioeconomic backgrounds and long term goals. It would make for more challenging discussion, but perhaps that’s for the better.

Using your example, sustainability might not be a key concern for someone in FatFIRE but I don’t know if removing discussion about sustainability from the group they’re in is really helpful for the greater good or even FatFIRE itself. Challenging them to sustainability concerns could, eventually, help incorporate that into their philosophy.

Similarly, the pollination can work backwards. Perhaps sustainability advocates would be more open to the internal motivations of FatFIRE folks once they have real discussions with each other and see them as real people.

It’s the group division and group think difficulty as old as time.

I have lost some interest in the movement after a job change – but I am also aware circumstances can change on a dime. We are in the gray area, but the dial will likely lean towards FAT FI in the next phase of my career.

Take care,

Max

Hey Max!

Thanks for stopping by. I’m sorry I missed this comment until now.

I’m hoping that job change and slight loss of FIRE interest is just indicative of you being in the “boring middle”, sort of just floating along and sorting out life. Nothing wrong with that.

After all, the entire point of all this FIRE stuff is just to enable you to spend more time…living life!

I love this post, because the more I learn the more I realize I don’t know and value learning from others. I have found over the years that FIRE has long preferred to be an echo chamber where each thinks they have the best, most optimized answer. Silos may be evolution especially as the FIRE voices diversify. I know my FIRE number has changed several times. Especially when my Grandma entered dementia care in her 80’s that cost more than double per month what her annual salary was when she retired in her 20’s (she lived there for over 7 years). Also when I learned my dad’s chemo cost 5k per month with the next level treatment at 10k monthly, plus having to hire people to do yard and other chores he used to do himself. Since all safe withdrawal rates are based on assumptions about future expenses and inflation, these experiences have been eye opening about how much I would rather work now to pad that number than to have to make future healthcare decisions based on cost affordability because my estimates were off.

Also, I love that I can type this comment without the page reloading multiple times from all the ads (and why I so seldom comment elsewhere)!

Marie—

I’m sorry to hear how much you’ve struggled with health difficulties within your family, not to mention the underlying healthcare costs. That’s terrible.

And you’re right, numerous horror stories cause Jenni and I to want to lean a little more on the safer side of things like the “4% rule” (of thumb). We’ve also tried to get familiar with alternative options for healthcare needs, including geoarbitrage.

Hopefully, down the road, we’ll just see an evolution of FIRE—perhaps something a little clearer for more people. An improvement. That’ll be better than dispertion.

And I’m glad you’ve enjoyed the [ad free] site! Mind you, this is what works for us and our goals. Plenty of authors out there do great and consistent work that deserve to be paid for their efforts. 🙂 Cheers!

Nice wise post. Thanks for writing it. I think I learn the most from people “a couple of doors down” (figuratively speaking), and building silos makes it harder to see them.

That’s why I like it when people write books… once I’ve gone to the trouble of getting something from the library, I’m willing to ride through some stuff that rubs me the wrong way, and then before you know it there’s a couple of useful nuggets. Whereas online, I skitter off at the first rough patch!

Ha, I get what you’re saying. Sometimes having something invested helps stick out the rough patches. It’s why some of those exercise programs work better when there’s a cost associated since folks don’t want to feel like they wasted money.

Similarly, deciding to buy (or checkout a book) involves a few of your decision points for that day and mental willpower to get going. You’re certainly more likely to give a shot than say, some little blog on the web that’s easy to hit the “x” on! 🙂

Glad you enjoyed the post, hope you stick around, Gerard. When you find something you don’t like, speak up! You’re probably not the only one and you might just help someone else (or the author!) out.